COVID-19 is uprooting economic globalization. With both supply and demand experiencing simultaneous shocks due to containment measures, global production networks are being disrupted on a scale never witnessed before. The pandemic has exposed how globally interconnected the flow of goods and services has become, and countries are now rethinking their international trade strategies to reduce their vulnerability to global economic shocks.

Disruptions to flows of foreign direct investments (FDI) — which are part and parcel of economic globalization — are no exception. In late March, the International Monetary Fund announced that investors had removed 83 billion US$ from developing countries since the beginning of the COVID-19 crisis, the largest capital outflow ever recorded.1 According to the UN Conference on Trade and Development (UNCTAD), global FDI flows are expected to contract between 30 per cent to 40 per cent during 2020/21. All sectors will be affected, but sharp contractions in FDI are especially evident in consumer cyclicals, such as airlines, hotels, restaurants and leisure, as well as manufacturing industries and the energy sector.2

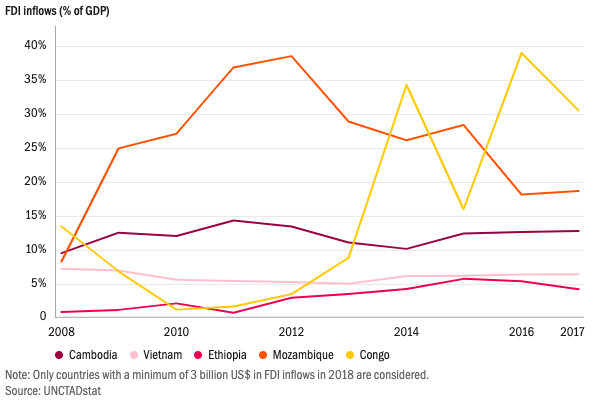

The contraction in FDI is going to hit developing countries particularly hard. The reasons for this are that first, FDI inflows to developing countries are expected to drop even more than the global average, considering that those sectors that have been severely impacted by the pandemic account for a larger share of FDI inflows in developing countries.3 Second, developing countries have become more reliant on FDI over the last few decades. FDI inflows to developing countries increased from 14 billion to 690 billion US$ (current prices) between 1985 and 2017. This represents an increase from 25 per cent to 46 per cent as a share of world FDI inflows. The increase in FDI to developing countries is underpinned by a rise in both offshoring and global fragmentation of economic activities, especially within the manufacturing and services sectors. The drop in global FDI is therefore very much related to the disruptions in global supply chains, which we have also witnessed as a result of the COVID-19 pandemic.